How to Calculate Estimated Useful Life of Asset

Useful Life Definition

Useful life is the estimated time period for which the asset is expected to be functional and can be put it to use for company's core operations and serves as an important input for calculating depreciation for assets which affects the profitability and carrying value of the assets.

How to Determine?

It is an estimation of a period until which the asset can be put to use, and it contributes to generating revenue. The following are the factors considered in determining it –

- Usage of the Asset – If the usage of the asset is more, then the useful life of the asset will reduce due to wear and tear, and it will get deteriorated rapidly.

- A newly procured asset will last longer than an already used asset since the same is already being put to use.

- When there are technological advancements, the asset will become obsolete as the same will no longer match the requirements of the current market.

- Any legal restriction, or any limits for the usage of the asset;

- The asset may last longer than it's estimated useful life, but the cost of maintenance of assets will considerably go high after a point of time. Over time the asset may become obsolete, and significant repairs can happen. It is determined based on how long the asset can be used before replacement.

You are free to use this image on your website, templates etc, Please provide us with an attribution link Article Link to be Hyperlinked

For eg:

Source: Useful Life (wallstreetmojo.com)

Useful Life of Equipment

Every asset has its period of usability, after which it cannot be put to use, or it will be obsolete. The useful life of assets will vary according to its nature, usage of the asset, company's replacement policy, etc.

There are estimations of available based on the nature of asset provided by the accounting body, Company can adopt the same for their assets, or they can make their assessment based on the proper asset valuation.

Impact on Depreciation

- Useful life is the estimated life of a depreciable asset until which it can be put to use for revenue-generating operations. It directly impacts depreciation expense as depreciation is calculated based on the number of years of assets life. More it is, lesser will be the depreciation and vice versa.

- Any change in it will alter the depreciation Depreciation is a method of accounting for the costs of any physical or tangible asset over the course of its useful life. Its value indicates how much of an asset's worth has been used. read more expense, and it will have an impact on the profitability of the business. If depreciation Depreciation is a method of accounting for the costs of any physical or tangible asset over the course of its useful life. Its value indicates how much of an asset's worth has been used. read more is more, the profitability Profitability refers to a company's ability to generate revenue and maximize profit above its expenditure and operational costs. It is measured using specific ratios such as gross profit margin, EBITDA, and net profit margin. It aids investors in analyzing the company's performance. read more will reduce. However, depreciation is a non-cash expenditure Non-cash expenses are those expenses recorded in the firm's income statement for the period under consideration; such costs are not paid or dealt with in cash by the firm. It involves expenses such as depreciation. read more , so the same will affect the cash flow of the business.

- Depreciation will be considered only when this life of the asset is more than a year. E.g., building, vehicles, etc. When an asset is procured, the entire cost of the asset is not expensed off as the same is capitalized, and it is depreciated over its useful life.

Examples of Useful Life

Below are the examples to understand the concept in a better manner –

E.g., .#1

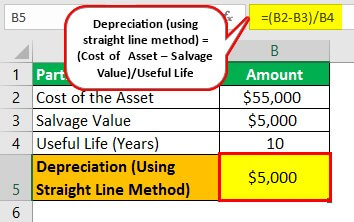

X Corp purchased a vehicle for transportation of its goods from its factory to the warehouse. The cost of the vehicle is $55,000, and it's expected useful life is 10 years and the salvage value is $5,000.

Solution

Calculation of depreciation will be as follows,

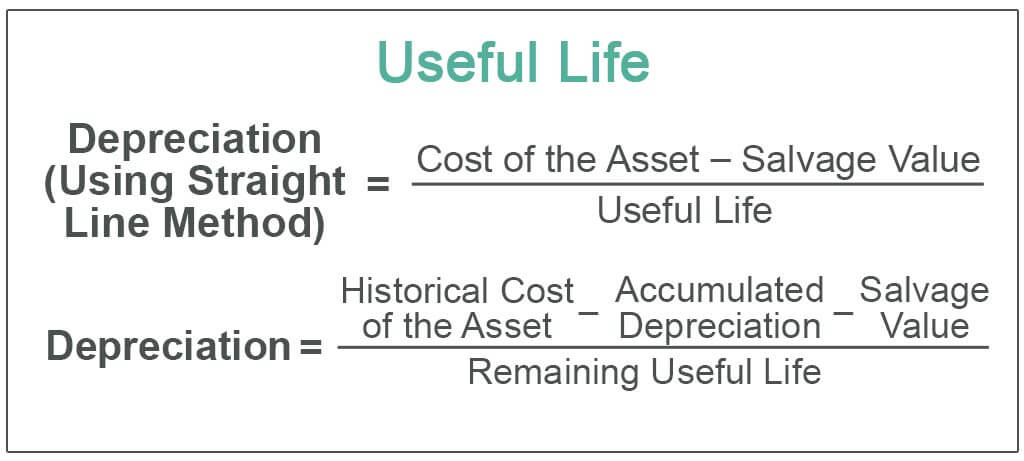

Depreciation under straight-line method Straight Line Depreciation Method is one of the most popular methods of depreciation where the asset uniformly depreciates over its useful life and the cost of the asset is evenly spread over its useful and functional life. read more = (Cost of the asset – salvage value)/ Useful life

- = ($55,000 -$5,000)/10

- = $5,000 per annum

So the impact of profitability on account of depreciation is $5,000 Per annum.

E.g., .#2

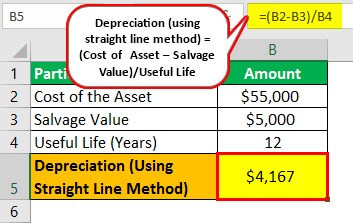

In case if the company estimates the useful life of the vehicle as 12 years with the same salvage value. So the revised depreciation calculation will be as follows:

Solution

Calculation of depreciation will be as follows,

Depreciation under straight-line method = ($55,000 – $5,000)/ 12

- Depreciation = $4,167 per annum.

So the impact on profitability will be $4,167 Per annum. There is an improvement in profitability to the extent of $833 per annum.

Change in asset's life or any revision is done prospectively, and for reported no of earlier years need not be changed. The prior period reported values need not be changed as it is not an accounting error Accounting errors refer to the typical mistakes made unintentionally while recording and posting accounting entries. These mistakes should not be considered fraudulent behaviour first-hand as this can happen with anyone and by anyone. read more , and it is an estimation, change in it is an inherent element.

E.g., #3

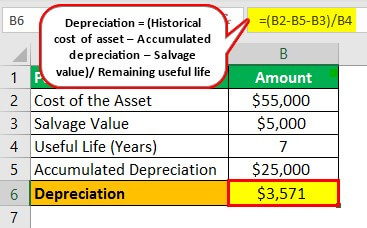

In the above case, if the revision of its useful life is done at the end of 5th year. The depreciation is already provided for 5 years as per 10 yrs. The depreciation provided is $25,000 ($5,000 Per Annum* 5 yrs). The book value of a vehicle will be $30,000 since life is revised as 12 years (i.e.) another 7 yrs instead of 5 yrs.

Solution

Calculation of depreciation will be as follows –

Depreciation = (Historical cost of the asset – Accumulated depreciation The accumulated depreciation of an asset is the amount of cumulative depreciation charged on the asset from its purchase date until the reporting date. It is a contra-account, the difference between the asset's purchase price and its carrying value on the balance sheet. read more – Salvage value)/ Remaining useful life

- = ($55,000 – $25,000 – $5000)/7

- = $3571 per annum.

The above depreciation is a non-cash expenditure, the cash outflow happened at the time of purchase of a vehicle, and there won't be any yearly impact.

For tax depreciation, it is an allowable expense, but the method of computation of depreciation is an accelerated method Accelerated depreciation is a way of depreciating assets at a faster rate than the straight-line method, resulting in higher depreciation expenses in the early years of the asset's useful life than in the later years. The assumption that assets are more productive in the early years than in later years is the main motivation for using this method. read more .

Difference Between Useful and Physical Life

- Useful life is the time period until which asset is effectively used in operations. In contrast, physical life is the time period till which the asset will be in physical form and after which it has no salvage value Salvage value or scrap value is the estimated value of an asset after its useful life is over. For example, if a company's machinery has a 5-year life and is only valued $5000 at the end of that time, the salvage value is $5000. read more .

- The physical life of the asset can only be known after the asset's life ends, whereas useful life will be determined even before the asset is put to use based on the usage, nature, and other factors. There can be many factors that make an asset unusable economically, but it will be physically available.

Conclusion

Useful life is an estimation and the actual life of the asset, maybe even more or it can less. It has to be considered after proper evaluation and considering all the factors. It is regarded as a critical element in asset recording and valuation as the depreciation and carrying value of the asset Carrying value is the book value of assets in a company's balance sheet, computed as the original cost less accumulated depreciation/impairments. It is calculated for intangible assets as the actual cost less amortization expense/impairments. read more depends on it, and it has a direct impact on profitability. It can always be revised considering the present technology, the asset being obsolete, higher usage, etc.

Recommended Articles

This article has been a guide to the Useful Life of an Asset and its definition. Here we discuss the useful life of the equipment, its impact on depreciation along with examples, and its differences from physical life. You may learn more about financing from the following articles –

- Accumulated Depreciation Journal Entry

- MACRS Depreciation

- Depreciation Rate

- Depreciation Tax Shield

How to Calculate Estimated Useful Life of Asset

Source: https://www.wallstreetmojo.com/useful-life/

0 Response to "How to Calculate Estimated Useful Life of Asset"

Post a Comment